“Retirees and Gen Z ultimately want the same things from work”

Our Public Affairs colleagues Sem Overduin and Oifik Youssefi co-authored the book *De ZZPuzzel*, a factual analysis of the self-employed issue. The book was the result of numerous discussions with labor market experts from academia, politics, and civil society. Persistent misinformation, one-sided perceptions, a lack of political decisiveness, and the complexity of labor law make this issue a complicated puzzle. In this series of articles, the authors engage in dialogue with stakeholders who contribute an additional piece of the puzzle.

Which puzzle piece would you like to add to The ZZPuzzle?

Ron van der Net: “If politicians and society believe that self-employed workers should contribute to social security, then make sure the system is fair and well-organized. A more equitable social security system would go a long way toward resolving the entire issue of eligibility.”

Marc Leene: “Right now, the discussion often gets bogged down in the question: are you an entrepreneur or an employee? Whereas the underlying question should really be how to effectively organize workers within the system. That’s still too often missing.”

In 2020, Statistics Netherlands (CBS) noted that an increasing number of people aged 65 and older are continuing to work after retirement. What do you think this trend indicates?

Marc Leene: “That says a lot. But there are plenty of retirees who want to keep working but don’t know how. There’s a huge pool of labor there that remains untapped.”

Ron van der Net: “There are also older people who work as self-employed professionals after reaching retirement age, but it should be noted that this group was already working as self-employed professionals before they retired. Incidentally, I no longer find the term ‘self-employed’ entirely appropriate. I prefer to refer to them as ‘those who enjoy the fruits of their labor.’ For this group, work is often no longer a primary necessity for survival, but rather something that provides fulfillment, rhythm, and meaning.”

In your opinion, what is the main reason why many retirees ultimately decide not to continue working?

Marc Leene: “Legislation and regulations, and entrenched ways of thinking. Employers often don’t understand how to deal with retirees. At the same time, many older people themselves aren’t aware of what’s still possible.”

Ron van der Net: “That is precisely why we place autonomy at the center. A retiree is no longer required to work. No one is forcing them to do anything anymore. That premise changes the entire relationship to work. Under the Continued Employment Scheme, we’re essentially saying: the autonomy of the continued employee is central. The continued employee retains the freedom to independently determine their workload, availability, and continuation of work. We then facilitate everything surrounding that. Think of payroll taxes, social security contributions, etc. We make the administrative process simple.”

Do you have any insight into the effects of continuing to work on the well-being and health of retirees?

Marc Leene: “Among workers participating in the Doorwerkregeling program, we see an attrition rate of about one percent. That is extremely low. We also see that people work an average of about 17 hours per week. This also shows that it’s not about working yourself to the bone well into old age.”

Ron van der Net: “Money is secondary for this group. After all, most of them have built up a pension and receive a monthly state pension. As a result, the role of work changes fundamentally. For many older adults, it’s no longer about employment conditions or building a career, but about finding meaning, maintaining social connections, and staying active.”

How significant do you think the contribution of people aged 65 and older is to addressing labor market shortages?

Ron van der Net: “It’s bigger than many people realize. The involvement of retirees can make a fundamental contribution to labor productivity, especially in sectors where experience, expertise, and reliability are important.”

Marc Leene: “For example, we launched the DoorwerkAmbtenaar initiative. Several municipalities reached out to former civil servants with the message: we have assignments that we simply can’t fill. People could reapply based on their experience and skills. That’s when you realize just how much knowledge is still out there.”

Do you view the Extended Work Program as a temporary solution in a tight labor market or as a long-term model for the future?

Marc Leene: “I really see it as a structural building block. We need to move away from the idea that retirement is some kind of final destination. Many people are simply retired and still working.”

Ron van der Net: “From a tax and legal perspective, this is still something of a rarity in the Netherlands. But from a societal standpoint, it has long been a reality.”

Marc Leene: “That’s why we try to explain to employers that they need to look at this group differently. Give people freedom. For example, accept that someone might turn down a job or want to work with short notice. Make it appealing and simple. Then it suddenly turns out not to be that complicated at all.”

In *De ZZPuzzel*, experts argue that the labor market needs to be overhauled to better reflect the changing reality of work. What are your thoughts on this?

Ron van der Net: “You have to look at the history of the labor market and ask yourself: where have we come from as a country, and where do we actually want to go? A reform of the social security system is essential in this regard. In addition, we have made many aspects of labor market qualifications unnecessarily complicated. Essentially, you want to work toward a transactional labor market: supply and demand are well aligned, the system is well-funded, and well-structured.”

When it comes to the labor market, what is your message to policymakers?

Marc Leene: “As Ron already mentioned, the labor market is unnecessarily complicated. This is partly due to politics. Employers who use the Continued Employment Scheme often say the same thing: keep it simple.”

Ron van der Net: “Issues like automatic retirement are often complex enough as it is. Ultimately, what people need most is clarity and simplicity. That applies to both employers and employees.”

Request a free consultation

Questions about this? Please contact us.

Sem Overduin

Public Policy & Affairs Manager

Sem.Overduin@headfirst.nl

Oifik Youssefi

Public Affairs Officer

Oifik.Youssefi@headfirst.nl

Maaike van Driel

Head of Legal

Maaike.vanDriel@headfirst.group

Thomas ten Veldhuijs

Senior Legal Counsel

Thomas.tenVeldhuijs@headfirst.nl

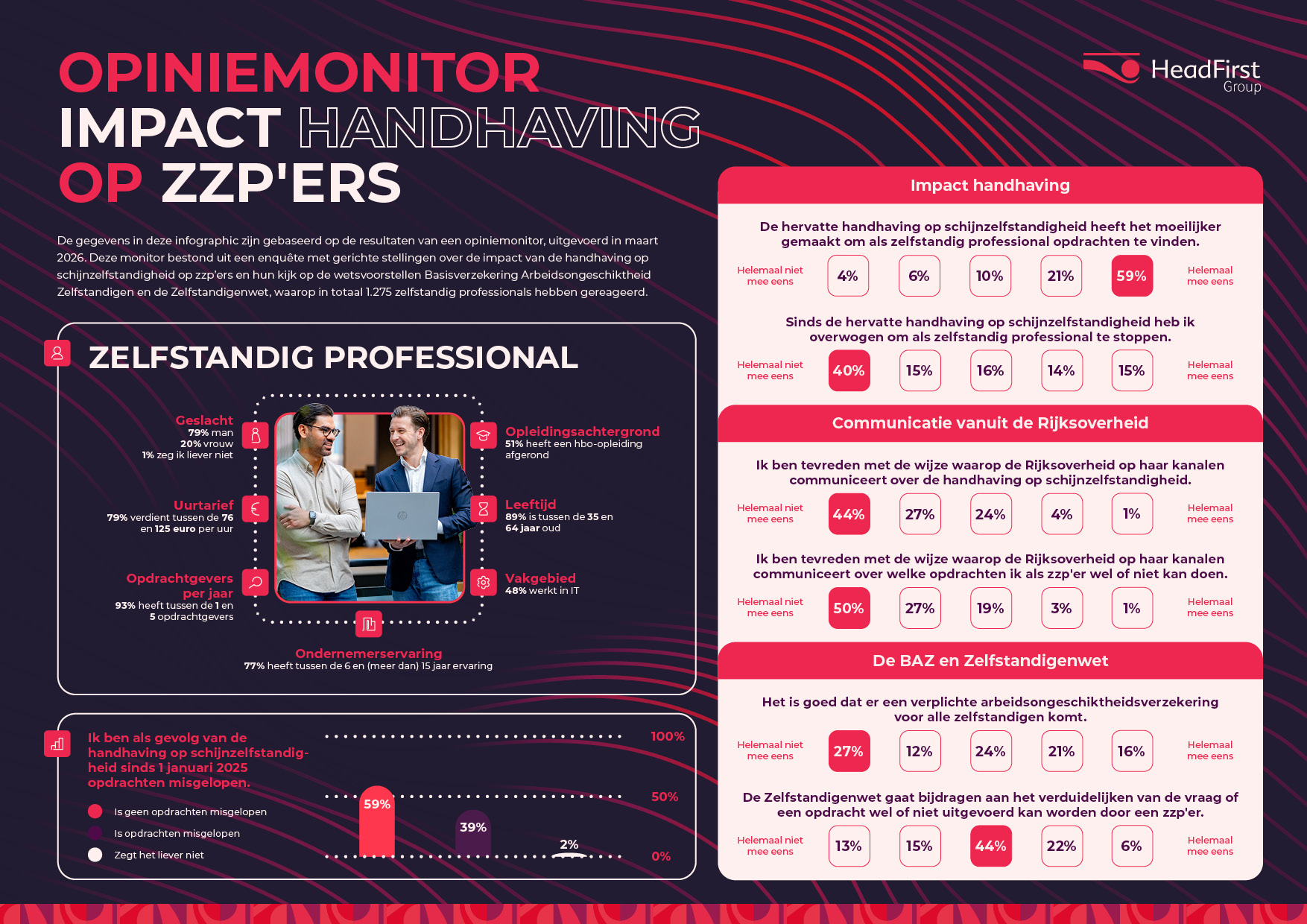

Opinion Monitor – Self-employed workers dissatisfied with the national government’s communication regarding the approach to bogus self-employment

The Jetten Cabinet is committed to clarifying the employment relationship between self-employed individuals and clients and to improving the position of self-employed individuals in the labor market. In doing so, the government is focusing, among other things, on the further development of two important legislative proposals: the Self-Employed Persons Act, a private member’s bill introduced by the VVD, CDA, D66, and SGP, and the Basic Disability Insurance for the Self-Employed (BAZ). At the same time, enforcement against bogus self-employment will continue.

Widespread dissatisfaction with the federal government's communication

As was the case in the 2024 Opinion Monitor, “uncertainty” is a key concern for many respondents. Despite the fact that nearly 69% are (very) well informed about the Tax and Customs Administration’s enforcement strategy, many self-employed individuals are worried. Given the amount of misinformation circulating on social media regarding enforcement against bogus self-employment, it is likely that there is a significant need for clear and consistent communication in advance.

Although the national government itself emphasizes the importance of clear communication regarding enforcement, over 70 percent of respondents say they are (very) dissatisfied with the way the government communicates on this issue. According to many self-employed professionals, uncertainty about the rules directly translates into fewer assignments. In HeadFirst Group’s 2024 opinion survey, self-employed professionals were also critical of the national government’s public campaign—in that case, regarding the lifting of the enforcement moratorium: 65% indicated that the campaign provided (absolutely) no clarity.

Politicians also took note of these concerns. Thierry Aartsen (VVD), now Minister of Labor and Participation, Hans Vijlbrief (D66), now Minister of Social Affairs and Employment, and then-Member of Parliament Mariska Rikkers-Oosterkamp (BBB) called on the previous cabinet in a motion to actively communicate that working with self-employed professionals remains possible, provided the rules are followed. This motion was adopted by the House of Representatives on May 27, 2025.

Nevertheless, there remains a great deal of uncertainty. Nearly 77 percent of respondents say they are (very) dissatisfied with the clarity regarding which assignments self-employed professionals can and cannot undertake.

Self-employed workers are not quite as enthusiastic about mandatory disability insurance (BAZ)

Respondents have mixed views on the further consideration of the Self-Employed Persons’ Basic Disability Insurance Act (BAZ), which was submitted to the House of Representatives for debate on Friday, March 13. On the one hand, nearly 38% say they think it is (very) good that mandatory disability insurance is being introduced; on the other hand, 39% say they think it is a (very) bad idea. A selection of the critical responses shows that self-employed individuals are concerned about the fact that coverage does not take effect until after two years and about “further government interference.” A large proportion also indicates that they can manage just fine on their own without mandatory disability insurance. Only 7% have made no provisions in case of disability. The rest do so through savings (59.4%), private insurance (50.4%), investments (39.5%), and finally, 10.9% are members of a bread fund. Although the bill aims to provide an opt-out for these cases, self-employed individuals without employees will still be required to pay a so-called stability contribution to the UWV. The amount of this contribution is currently unknown and is being further developed by the government.

Ook de Zelfstandigenwet geniet geen brede steun

Only 27.7 percent of respondents are (very) convinced that the Self-Employed Persons Act will actually help clarify whether or not a particular assignment can be carried out by a self-employed person. That is a striking finding.

In April 2025, a survey conducted by Knab revealed that a large majority of self-employed individuals view the private member’s bill for the Self-Employed Persons Act favorably. A survey of more than 7,500 self-employed entrepreneurs showed that 71 percent would support the proposal if they were members of the House of Representatives.

That is a strikingly high percentage, especially for a law that may also introduce new obligations for self-employed individuals, such as arranging for a pension and disability insurance. In the survey, 17 percent said they opposed the proposal, while 12 percent were still undecided.

Handhaving en wetgeving zetten zzp-markt onder druk

The results of this opinion survey paint a stark but clear picture of the sentiment among highly educated self-employed professionals regarding the resumption of enforcement against bogus self-employment and potential legislation. Many respondents are already experiencing the tangible effects of this enforcement in the form of fewer available assignments.

Furthermore, the results show that uncertainty regarding whether a self-employed person can or cannot accept a contract plays a significant role in current market developments. Despite a relatively high level of awareness of the Tax and Customs Administration’s enforcement strategy, many self-employed individuals indicate that the market turmoil is leading to caution among clients. According to respondents, this directly translates into fewer contracts.

Opinions on the new legislation also remain mixed. Both the mandatory disability insurance and the Self-Employed Persons Act are eliciting mixed reactions. While some self-employed individuals view the proposals as a step toward greater security and clarity, a significant portion questions their effectiveness, particularly when it comes to actually eliminating uncertainty regarding the use of self-employed workers. On a positive note, 93% of respondents have made provisions for disability, and 94% for retirement.

The findings thus underscore the importance of clear and consistent communication regarding the applicable rules and the purpose of enforcement. In a labor market where self-employed professionals play a significant role, predictability is essential for both clients and self-employed professionals. Especially during this phase of potential changes in policy and legislation, a clear explanation of what is and is not permitted can help foster greater confidence and stability in the market.

Request a free consultation

Questions about this? Please contact us.

Sem Overduin

Public Policy & Affairs Manager

Sem.Overduin@headfirst.nl

Oifik Youssefi

Public Affairs Officer

Oifik.Youssefi@headfirst.nl

Maaike van Driel

Head of Legal

Maaike.vanDriel@headfirst.group

Thomas ten Veldhuijs

Senior Legal Counsel

Thomas.tenVeldhuijs@headfirst.nl

“Entrepreneurship is freedom, but without individual responsibility, the system doesn’t work.”

Public Public-colleagues Sem Overduin and Oifik Youssefi co-authored the book The ZZP Puzzle, a factual account of the self-employed issue. The book was the result of numerous discussions with labor market experts from academia, politics, and civil society. Persistent misinformation, one-sided perceptions, a lack of political decisiveness, and the complexity of labor law make this issue a complicated puzzle. In this series of articles, the authors engage in conversation with stakeholders who contribute an additional piece of the puzzle.

Which puzzle piece would you like to add to The ZZPuzzle?

The individual responsibility of self-employed workers. I don’t see this reflected enough in the discussion surrounding self-employment. Remember: if you don’t make provisions for disability or retirement, something is going wrong. Entrepreneurship also means looking ahead.

As far as I’m concerned, tax benefits should be made conditional. Consider the SME profit exemption or the self-employed tax deduction. Attach requirements to them. If you haven’t made the necessary provisions, why should you receive all the benefits? Both schemes are currently being significantly scaled back, but otherwise that would have been a worthy goal.

Many self-employed individuals are concerned about the changes to Box 3. To what extent is the current uproar, according to you based on actual risks, and to what extent on misinformation or framing?

Keep it simple: compare the current situation with what it will become. Right now, you pay taxes on a notional return. That’s fundamentally unfair, because it says nothing about what you’ve actually earned. So the move to taxing actual returns makes perfect sense.

The debate mainly centers on illiquid investments. Cryptocurrency has often been cited as an example lately, but the problem is being exaggerated in that context. If you have a profit, you can cash out a portion of it and use that to pay your taxes. That’s not an insurmountable hurdle.

The situation is more complex when it comes to assets that cannot be easily liquidated, such as real estate. In such cases, the basic principle is rightly different: tax is only levied when you actually sell the asset and realize the profit.

The basic principle is clear. You can tax liquid returns immediately. Non-liquid returns are taxed at the time of realization. That distinction actually makes the system more consistent.

The outrage often stems from a lack of clarity or how the issue is framed. Fundamentally, less is changing than is suggested. You will still pay taxes on unrealized gains—just as you do now—only no longer on a hypothetical amount but on what you have actually earned.

NOS reportreported reported in February that pension providers are seeing increased interest from self-employed people due to the new Box 3 rules. See Do this as a temporary reaction to the revision plans, or does it point to a structural shift in how self-employed people view their pensions?

In fact, every year we see an increase in the number of self-employed individuals registering compared to the previous year. This year, however, the increase has been significantincrease. I wouldn’t dare say whether this marks a structural shift. What is certain, however, is that there is a knowledge gap. A large proportion of self-employed individuals don’t even know that they can build up a tax-advantaged pension in Box 1. Most of them are still saving in Box 3.

That’s really the crux of it. In Box 1, you can make contributions and deduct them from your income tax, and you pay the capital gains tax. That’s actually much more advantageous. The reporting on this topic is often misleading. It seems as though Box 3 is the go-to option for entrepreneurs’ pensions, but that’s not true.

The announcement by Eelco Heinen (VVD), Minister of Finance, to revise Box 3 on a number of points, without broad consultation, drew a lot of criticism. What does such a spontaneous change of course mean, according to you do you think such a sudden change of course does to the confidence of self-employed professionals in politics regarding this issue?

I do think that’s generally a problem. In terms of continuity, this is undesirable. Just look, for example, at the debate surrounding the increase in the retirement age. A few years ago, the pension agreement stipulated that the increase would be slowed down, and yet the new coalition is deviating from that again. That undermines trust.

The same is true for Box 3. That issue has been dragging on for years and hangs over the market like a sword of Damocles. Everyone understands that the current system is unsustainable and that something needs to be done, but the lack of consistency makes it unpredictable. Continuity is crucial here, and it makes sense that self-employed individuals have become more critical as a result.

In addition, there is valid criticism of the way losses are handled, particularly the carryforward and carryback provisions. If you get that right and at the same time move away from the notional return, you essentially have a workable system.

The plans for the proposed Self-Employed Persons Act discuss making pension plans for self-employed individuals. To what extent does do you this requirement necessary for self-employed individuals?

From a business perspective, it would be interesting for us—I’ll be honest. Entrepreneurship isn’t just about freedom; it’s also about responsibility. At the same time, as a matter of principle, I’m not in favor of legal obligations.

The bill refers to “adequate provisions,” but what that means in concrete terms remains unclear. Everyone already contributes to the AOW; that much is clear. In my view, the focus should be on ensuring that self-employed individuals not only save for the future, but also have the means to enjoy the present.

If someone runs into financial difficulties, and this is clearly evident in their income tax return, it should be possible to withdraw funds early from a savings account set aside for later use. Currently, this is only allowed in cases of long-term disability.

Relax those rules. Make sure people can access their retirement savings sooner if necessary. The COVID-19 crisis has shown why this is essential. Many self-employed people had to dip into their own savings at the time. You need to take this seriously when designing the system.

Employees accrue pension benefits through group plans, while self-employed individuals must arrange their own coverage. In a labor market where people are increasingly switching between salaried employment and self-employment, critics argue that this distinction is becoming increasingly problematic. Where does this system begin, according to you ?

Pension systems in the Netherlands should, at their core, be individual-based. Under the old system, which utilized the Financial Assessment Framework, the emphasis was strongly on security. As a result, a significant amount of collective assets was accumulated, with a portion of those assets tied up in buffers to provide that so-called security.

The Future Pensions Act is changing that, but the structure is still partly based on a labor market that no longer exists. In the past, people often worked in a single sector for a long time, which was linked to a single pension fund. That model is becoming increasingly out of step with reality. The average 35-year-old already has about five pension plans.

Workers now move much more frequently between employers or clients, across sectors, and between different types of contracts. In this context, a system tied to employers simply makes less sense. By making pensions truly individual-based, they become neutral with respect to the form of employment. This better aligns with how people work today and ensures continuity, regardless of the form of employment.

Experts, including those in the book, generally advocate for a reform of the social security system in which both salaried employees and self-employed individuals contribute to pensions and disability insurance, among other things. What is your view you on this?

I am a strong advocate of this. Every working person should contribute to social security. That makes the system fairer and more widely supported.

There is a risk involved, though. If you’re a self-employed professional and temporarily don’t have any assignments or aren’t making a profit, it becomes difficult to make contributions. That requires flexibility in how you manage your finances.

That is precisely why personal responsibility remains essential. As a self-employed person, you need to build up a financial cushion and set aside savings so that you can stay afloat even during leaner times.

In closing, what is your advice to politicians in The Hague?

Ensure that self-employed individuals—in the event of financial hardship—can access their annuity funds sooner. Not to undermine the system, but to lower the barrier to saving money.

The point isn't that people should drain their retirement savings, but that this option is available in exceptional circumstances. The pandemic has shown that this need is very real.

It is precisely that flexibility that can convince people to start building up savings through Box 1. Thanks to the recent expansion of Box 1, people can also set aside much more, making it easier to use that buffer for other financial emergencies. A self-employed person certainly wants a nest egg, too. It’s just that for a self-employed person, that need can strike much sooner and at unexpected moments!

Request a free consultation

Questions about this? Please contact us.

Sem Overduin

Public Policy & Affairs Manager

Sem.Overduin@headfirst.nl

Oifik Youssefi

Public Affairs Officer

Oifik.Youssefi@headfirst.nl

Maaike van Driel

Head of Legal

Maaike.vanDriel@headfirst.group

Thomas ten Veldhuijs

Senior Legal Counsel

Thomas.tenVeldhuijs@headfirst.nl

No, earning more than 38 euros per hour doesn't automatically make you a self-employed person

If it were up to Thierry Aartsen (VVD), Minister of Labor and Social Inclusion, the government would move quickly to introduce a legal presumption of employee status below a certain hourly rate. Aartsen Aartsen announced on Friday, March 6 to to the House of Representatives. Self-employed workers earning less than 38 euros per hour will then be able to more easily claim to an employment contract. But as is often the case with the self-employed issue, this proposal faces a persistent misunderstanding. On social media, the perception is circulating that there will be a strict cutoff: below 38 euros per hour you are an employee, above that you are by definition a self-employed person. In short: this isn’t true, and it’s important to know why that is.

Why “refutable” is the key word

The legal presumption is therefore rebuttable. This means that the client, in turn, can rebut the presumption by presenting specific facts and circumstances that indicate self-employment.

The judge then considers all the circumstances of the case. These include the degree of authority and supervision, the employee’s organizational placement, the business risk, and the nature and duration of the work.

As noted earlier, the result is that even if the hourly rate is below 38 euros, the individual may still be considered a self-employed person, since the relevant facts and circumstances remain the determining factor in assessing the employment relationship. There is therefore no automatic transition to employee status.

What happens above 38 euros

The finding that you’re “safe” above 38 euros are “safe” as a self-employed person is therefore incorrect. Above that threshold, the legal presumption does not apply. That is basically all there is to it. There is no such thing as a “legalpresumption of independence’. The holistic test – based on the perspectives of the Deliverooruling and the constantly evolving case law – remains exactly the same as. This means that even with higher rates, an employment contract may still exist if the factual circumstances indicate so. The rate is not a decisive criterion, but merely one element among many.

Who is this for?

According to ZiPconomy , a significant number of self-employed professionals work below the 38-euro-per-hour threshold. About 60 percent of all self-employed professionals (if hired at 38 euros per hour) could, in theory, take advantage of this law. This is evident from a calculation by the Ministry of Social Affairs and Employment based on figures from the Self-Employed Labor Survey (ZEA) conducted by CBS and TNO. This applies to sectors where rates are structurally lower, such as agriculture, hospitality, and transportation and warehousing.

At the same time, it appears that many of these workers consciously choose self-employment and do not necessarily wish to claim all the rights and social protections that come with an employment contract. This underscores that the legal presumption is not an obligation, but a legal tool that can be utilized. The legal presumption does not alter the definition of a self-employed person or an employee. Anyone who understands this clearly will see that there is little reason for panic (or misplaced joy in the case of self-employed individuals with higher hourly rates).

On Wednesday, April 15, there will be a debate will take place in the House of Representatives. The House Committee on Social Affairs and Employment will debate the labor market and self-employed workers dossier.

Request a free consultation

Questions about this? Please contact us.

Sem Overduin

Public Policy & Affairs Manager

Sem.Overduin@headfirst.nl

Oifik Youssefi

Public Affairs Officer

Oifik.Youssefi@headfirst.nl

Maaike van Driel

Head of Legal

Maaike.vanDriel@headfirst.group

Thomas ten Veldhuijs

Senior Legal Counsel

Thomas.tenVeldhuijs@headfirst.nl

Certainty in advance is not possible, but we must strive for greater clarity.

In the discussion about the use of freelancers, one question dominant: can this assignment be carried out by a self-employed person or not? During the book launch of De ZZPuzzel , a panel consisting of Connie Maathuis, Niels van der Neut, and Hugo Jan Ruts whether more certainty can be provided in advance to clients and self-employed professionals. The panel showed that complete certainty sounds appealing, but that this is not possible in practice.

European regulations

University lecturer in labor law Niels van der Neut at the University of Amsterdam explained that national legislation should also take European legislation. "You can say at the national level that someone is a freelancer, but under European law can that same person still qualify as an employee." Ultimately, every situation must be assessed on the basis of "all circumstances of the case" .. Exactly as prescribed by European labor regulations and as the Supreme Court has repeatedly has . It remains a matter of holistic assessment.

Belgium as an example? Only with nuance

Although Belgium has a system in which independence for certain professional groups is assessed using sectoral criteria, in practice this is limited and rarely used. Van der Neut and Ruts warned against idealizing this system. In Belgium, only a few cases per year are submitted to the Administrative Commission for the Settlement of Labor Relations, a review committee that, in cases of doubt, examines the labor relations. In addition, Belgian self-employed persons are compulsorily insured against, for example, incapacity for work and therefore contribute to a social security system, which reduces the pressure on the qualification question.

Phased introduction increases uncertainty

Connie Maathuis, chair of VZN, warned further that the phased introduction of the Self-Employed Persons Act can can cause uncertainty. "Don't go for a phased implementation. The market urgently needs more clarity," she said.

Complete certainty at the outset is impossible. The employment relationship test is holistic in nature, takes all circumstances of the case and will take place retrospectively. In a rapidly changing labor market, there must therefore also room for customization and there always take into account European regulations.

Request a free consultation

Questions about this? Please contact us.

Sem Overduin

Public Policy & Affairs Manager

Sem.Overduin@headfirst.nl

Oifik Youssefi

Public Affairs Officer

Oifik.Youssefi@headfirst.nl

Maaike van Driel

Head of Legal

Maaike.vanDriel@headfirst.group

Thomas ten Veldhuijs

Senior Legal Counsel

Thomas.tenVeldhuijs@headfirst.nl

“Sectoral minimum rates for self-employed workers in principle solve the problem of bogus self-employment”

Public Affairscolleagues Sem Overduin and Oifik Youssefi wrote together the book The ZZPuzzel, a factual account of the self-employed dossier. The book came about after many discussions with labor market experts from the science, politics, and civil society. Persistent misinformation, one-sided image formation, lack of political decisiveness, and the complexity of labor law make the dossier a complicated puzzle. In this series of articles, the authors talk to stakeholders who contribute an additional piece to the puzzle.

To what extent do you think the self-employed dossier is a puzzle?

For me, this issue has been a puzzle for years. Since the introduction of the DBA Act, we have been grappling with the same problem: the employment relationship test. This is partly due to weak representation of the interests of self-employed people and partly due to strong lobbying from the business community. This makes it difficult to arrive at a balanced solution. The call for more clarity about the employment relationship has been heard for years, but the basis of the self-employed population often remains out of sight.

I have long been preoccupied with the question of what is fair for self-employed professionals. For me, the solution lies in sector-specific minimum rates, enshrined in law. That addresses the core of the problem.

The book examines the issue from perspectives such as misinformation, image formation, and political decisiveness. Which piece of the puzzle do you think is decisive?

"Political decisiveness. We have known for years that there is a problem, especially at the grassroots level of the market. People who structural struggle to make ends meet because rates are under pressure. Without political will, nothing will change. You can discuss it endlessly discuss about authority and entrepreneurship, but as long as you do nothing about the income position of vulnerable self-employed people, the problem will remain."

Which puzzle piece would you add to The ZZPuzzle?

“I prefer to solve the puzzle. Sector-specific minimum rates can get you a long way. Not a single generic limit, but lower limits calculated for each sector that correspond to the average number of billable hours and cost structure.

It is important that these rates are not optional. You can make them legally binding or link them to access to supplementary social security. This creates an incentive to operate within reasonable margins. Enforcement could, for example, be entrusted to the Labor Inspectorate.

You argue in an article on ZiPconomy for sectoral minimum rates for self-employed professionals. What is the core problem you want to solve with this?

A minimum rate is not a standard price, but a lower limit, comparable to the minimum wage for salaried employees. Below that level, it is not economically realistic to operate sustainably as a self-employed person.

In practice, self-employed people sometimes work at rates that are unsustainable, due to competitive pressure or a weak negotiating position.

My proposal addresses several problems at once: competition between employees and self-employed workers, bogus self-employment, lack of provision for retirement and disability, and poverty among self-employed workers.

Many people only look at the hourly rate, but forget that self-employed people cannot claim all their hours. If an editor works 37 hours, of which an average of 23 hours are billable, the rate must be calculated in such a way that, after deducting non-billable hours and costs, the editor earns at least the minimum wage. This requires a calculation per sector, not a single generic limit.

Wouter Koolmees attempted as Minister of Social Affairs and Employment in the past to introduce a minimum rate, but that proposal was rejected. Why would your idea work?

Koolmees' proposal was based on a single fixed rate. My proposal works with brackets, based on billable hours per professional group. This brings you in line with the reality of the sector.

A fixed limit, such as the €16 proposed at the time, does not do justice to differences between, for example, media, culture, or technology, and flattens everything. If you don't take those differences into account, it's not surprising that such a proposal doesn't make it.

Critics argue that a minimum rate reduces the scope for negotiation. What is your response to that?

That space is indeed shrinking. But right now, that space is so large that in some markets it is taking on antisocial proportions. The only thing that is no longer negotiable is a price level that drives people into poverty and makes it impossible to build social security. Everything above that remains negotiable. Currently, the risks lie entirely with the self-employed, while clients benefit from low rates.

A minimum wage makes the market more socially responsible. A recent motion by Mirjam Bikker (Christian Union), among others, calling on the cabinet to ensure that poverty figures do not rise during this cabinet term, was supported by the entire House of Representatives. All coalition parties also voted in favor.

Just as employees cannot be paid less than the minimum wage, self-employed people should also have a minimum income base. If you multiply the average number of billable hours by standard rates, in some sectors you end up with an annual income well below the minimum.

How does your idea for sectoral minimum rates relate to the legal presumption of employment, as proposed in the Clarification of Employment Relationships and Legal Presumption Bill?

The legal presumption is based on an hourly rate of €38 in 2026, accrued minimum wage, pension, disability insurance, and adjustment for non-billable hours. However, the percentages used are fixed, whereas in practice they vary per sector.

Some self-employed people will benefit from such a legal presumption. But that fixed limit is too generic. There are sectors in which people work for less than €38 and are clearly entrepreneurs.

At the same time, there are professions in which €38 is insufficient to exceed the minimum wage, given the limited number of billable hours per year. Some professions only have 700 to 1,000 billable hours per year. In that case, €38 is not much. So you have to look at the economic reality of a sector, and that is diverse.”

How do you view the bill? Self-Employed Persons Act, which the new cabinet is focusing on?

Clarifying the employment relationship is a positive step. However, if you simultaneously introduce obligations for disability and retirement without addressing low rates, you are placing the burden on the most vulnerable group. That is a blind spot.

If you calculate the lower limit correctly, self-employed people are by definition more expensive than employees, and price competition ceases to exist. This makes the type of contract less decisive.

What advice would you give to politicians?

Take sector-specific minimum rates seriously. Look at each market individually to determine what is needed to ensure that self-employed people earn at least the minimum wage. This will tackle bogus self-employment and prevent price competition between self-employed people and employees. It also creates financial scope for disability insurance and pension accrual.

In addition, technological developments such as AI will only increase the pressure on rates. Without a minimum threshold, poverty among the self-employed will continue to grow. Politicians have already stated that this must not be allowed to happen. Now it is time for action.

Request a free consultation

Questions about this? Please contact us.

Sem Overduin

Public Policy & Affairs Manager

Sem.Overduin@headfirst.nl

Oifik Youssefi

Public Affairs Officer

Oifik.Youssefi@headfirst.nl

Maaike van Driel

Head of Legal

Maaike.vanDriel@headfirst.group

Thomas ten Veldhuijs

Senior Legal Counsel

Thomas.tenVeldhuijs@headfirst.nl

The rise of the self-employed is a response to a labor market that does not work for everyone.

The political debate about self-employed workers often focuses on the risks, vulnerable workers, and potential abuses. During the book launch of De ZZPuzzel in Nieuwspoort, a three-member panel—Connie Maathuis, Niels van der Neut, and Hugo Jan Ruts — presented a different picture: many professionals consciously and wholeheartedly choose self-employment. Not out of necessity, but as a well-considered career choice. Self-employment is not a temporary trend or escape route; it is an integral part from the labor market in 2026.

Self-employed persons as indispensable link in the social system

The panel stated that self-employed persons may be part be be part of the collective social security system. Not for protection, but for the affordability of the system. This could ease the pressure on the qualification question, because there are significant differences in social security and taxation between contract.

A healthy labor market requires room for independent entrepreneurship.

The panel was unanimous: the self-employed professional is here tostay stay, but there is still work to be done to give the self-employed a solid position in the labor market. This means that a substantive debate must be held on the future of the labor market and the position of the self-employed in social security and taxation. In any case, the time for sticking plasters is over. Maathuis warned that uncertainty, for example in legislation, affects not only the self-employed, but also clients and the economy: "Uncertainty inhibits innovation, flexibility, and labor mobility. Autonomy only works if the environment supports it."

According to the panel, self-employed professionals are therefore are professionals who believe in freedom, responsibility, and entrepreneurship. This group deserves clear legislation, a fair position in the social system, and a full voice in labor market policy. Self-employment is no longer an exception; it is the labor market.

Request a free consultation

Questions about this? Please contact us.

Sem Overduin

Public Policy & Affairs Manager

Sem.Overduin@headfirst.nl

Oifik Youssefi

Public Affairs Officer

Oifik.Youssefi@headfirst.nl

Maaike van Driel

Head of Legal

Maaike.vanDriel@headfirst.group

Thomas ten Veldhuijs

Senior Legal Counsel

Thomas.tenVeldhuijs@headfirst.nl

SER 3.0 brings self-employed workers to the table on a structural basis

The position of self-employed people in the Netherlands remains a topic of discussion. Increasingly, the question is being asked whether the current polder model is still appropriate for a labor market in which self-employed people play a structural role. This discussion was the focus of a panel with Connie Maathuis, Niels van der Neut, and Hugo Jan Ruts at the book launch ofDe ZZPuzzel(The Self-Employed Puzzle) in Nieuwspoort. The conclusion was crystal clear: the traditional polder model is in need of reform.

Why the polder itself must change

The panel emphasized that change must not come solely from politics. The polder—employers' organizations, industry associations, and trade unions—must also structurally recognize the self-employed as an important pillar of the labor market. Three pain points emerged clearly:

- Self-employed individuals are an essential part of many sectors, from IT and healthcare to business services.

- The traditional "employee versus employer" model no longer fits in with a labor market in which hundreds of thousands of professionals consciously choose independence.

- Self-employed people are still too often only invited to the table "by invitation," which limits their influence.

The panel therefore advocated for a SER 3.0, in which self-employed persons are fully-fledged and structural discussion partners.

Power and responsibility

Niels van der Neut, assistant professor of labor law at the University of Amsterdam, pointed out an uncomfortable truth: a permanent place for self-employed workers means that traditional parties will have to relinquish power. This raises difficult questions:

- Who decides which self-employed organizations are invited to the table?

- What does this mean for the influence of employer and employee representatives?

- Who dares to really set the reform process in motion?

Van der Neut: “The polder will not do this on its own. Parties must voluntarily relinquish power — something that rarely happens spontaneously. It requires political choices and administrative courage.”

The SER model 3.0: contours of change

According to the panel, a modern SER model should meet the following criteria:

- Self-employed persons have a permanent seat at the table.

- Not as a side seat, but as a fully-fledged third party.

- Broad social representation carries more weight than historical structures.

- Decisions affect employees, employers, and self-employed persons.

This requires institutional reform and a change in mindset: self-employed people should no longer be "invited to join in."

Timing and urgency

With a new cabinet on the horizon and a different approach to the self-employed issue, the topic is back in the spotlight. A future-proof labor market starts with recognition, representation, and a transparent structure in which all workers—permanent, flexible, and self-employed—can truly participate.

Request a free consultation

Questions about this? Please contact us.

Sem Overduin

Public Policy & Affairs Manager

Sem.Overduin@headfirst.nl

Oifik Youssefi

Public Affairs Officer

Oifik.Youssefi@headfirst.nl

Maaike van Driel

Head of Legal

Maaike.vanDriel@headfirst.group

Thomas ten Veldhuijs

Senior Legal Counsel

Thomas.tenVeldhuijs@headfirst.nl

Book launch De ZZPuzzel: "Now is the time for political courage"

The self-employed worker issue remains one of the most persistent labor market puzzles. Politicians, policymakers, and practitioners have been trying for years to get a handle on the question of when a job can be performed by a self-employed person. With De ZZPuzzel (The Self-Employed Puzzle), Sem Overduin and Oifik Youssefi (HeadFirst Group) present a factual and accessible analysis of this issue. It is a subject that has rarely been so multifaceted and changeable.

Legislation helps, but does not solve everything

Labor lawyer Niels van der Neut emphasized that lawyers are keen to examine the self-employed issue, but that "this does not always work out favorably for self-employed people who just want to work." He warned that the debate has become too fixated on the question of classification, while the fundamentals—the social and tax systems—are at least as important. Van der Neut also tempered expectations regarding absolute clarity in advance. European law makes it impossible to provide completely watertight prior assessment. At the same time, he does see room for improvement: the better the tax and labor law criteria are developed, the less uncertainty there will be afterwards.

“Political decisiveness is needed now more than ever”

For Connie Maathuis, chair of the Dutch Association of Self-Employed Persons (VZN), the task facing the new cabinet is crystal clear. She believes that the prospective Minister of Labor and Participation, Thierry Aartsen (VVD), in particular, has a heavy responsibility.Political decisiveness is now more necessary than ever," Maathuis stated. She warned that a phased introduction of legislation—such as in the case of the legal presumption of employment—will primarily lead to additional uncertainty in the market.

According to her, there is a need for clarity in one go, including through the further elaboration of the Self-Employed Persons Act and the rapid introduction of parts of the bill on Clarification of the Assessment of Employment Relationships and Legal Presumption (VBAR). "Don't give self-employed persons and clients yet another period of uncertainty."

Legal presumption: nuance is needed

Van der Neut also examined the legal presumption of employment. He emphasized that it is primarily a procedural law support for self-employed persons with low rates: "It is not a prohibition to work as a self-employed person below a certain rate, and the underlying criteria remain exactly the same." This is a persistent misunderstanding that he wanted to dispel emphatically.

The polder must start moving on its own

Maathuis also pointed out that self-employed people are still not a natural part of the traditional polder model. "We have a seat at the table, but it's not yet our seat," she said. In her view, broad and structural representation of self-employed people should not be a favor, but a logical consequence of the current labor market.

The panel agreed that a 'SER model 3.0' is not an unnecessary luxury: a polder that moves with a reality in which self-employed people play a structurally significant and lasting role.

2026 will be a year of choices

The core message of the afternoon was clear: doing nothing is no longer an option. The self-employed dossier requires direction, political courage, and consistency. Ruts put it bluntly by stating that the alternative to action is simply "doing nothing"—and that no one in the labor market wants that anymore.

Request the ZZPuzzle

Would you like to read all the analyses, background information, and possible solutions yourself? Request De ZZPuzzel free of charge via this page: https://content.headfirst.group/zzpuzzel-aanvragen/

New book lays out the pieces of the puzzle surrounding self-employed workers

The new book De ZZPuzzel (The Self-Employed Puzzle) is being published at a time when the discussion about the position and role of self-employed professionals in the labor market is once again in the spotlight. Clear political choices have been made in the recently published coalition agreement, and since the end of the enforcement moratorium on January 1, 2025, there is still uncertainty among self-employed people and clients. Research cited in the book shows that a significant proportion of self-employed people are noticing a decline in assignments and that organizations have become more cautious about hiring self-employed professionals.

A labor market that has outgrown the system

What De ZZPuzzel also reveals is that the real problem lies deeper than legislation or enforcement. Dutch labor law and the social security system were designed at a time when work was almost exclusively carried out in salaried employment. The rise of hybrid careers, project-based work, and self-employment is increasingly difficult to fit into legal categories. This creates tension between different interests, such as individual freedom of choice, collective protection, solidarity, and the sustainability of the social security system. According to the authors, this explains the importance of taking an integrated view of the self-employed issue. As long as the system itself is not revised, any measure will be merely a band-aid solution. A much more fundamental reform is therefore necessary.

The self-employed do exist

Although it is often claimed that "the self-employed person does not exist," the book convincingly demonstrates that the self-employed person is indeed a recognizable worker. Although the group is very diverse, the initial motives are generally clear, the number of forced self-employed persons is small, and the majority of self-employed persons are very satisfied with their working conditions.

The authors demonstrate how simplifying this group not only obscures the debate, but also has consequences for the development of policy and legislation. As a result, the political discussion remains stuck in extremes, while the reality is much more nuanced.

How did it work again?

The ZZPuzzle does not advocate a ready-made solution, but it does lay out the pieces of the puzzle in order to gain a better understanding of the self-employed issue. According to the authors, the debate can only move forward when there is broader recognition of the key question: how do we organize freedom of choice, social protection, and collectivity in a labor market in which contract forms are becoming blurred, workers' preferences are changing, and workers are increasingly difficult to pigeonhole? According to the authors, it is very important that this fundamental debate takes place in The Hague.

A future-proof labor market requires political choices that extend beyond a single term of office and go beyond the reflex to keep building new rules on a foundation that has become unstable.

The book demonstrates that progress is only possible when all parties involved—politicians, government, social partners, market players, and the self-employed—share the same facts, the same history, and the same social context. Only then can there be room for policies that are feasible, fair, and future-proof.